Share buybacks

A bad practice or a win-win for companies and investors?

2024 is set to be a banner year for share buyback programmes. But many market participants are critical of this practice - despite the strong endorsement from Warren Buffett.

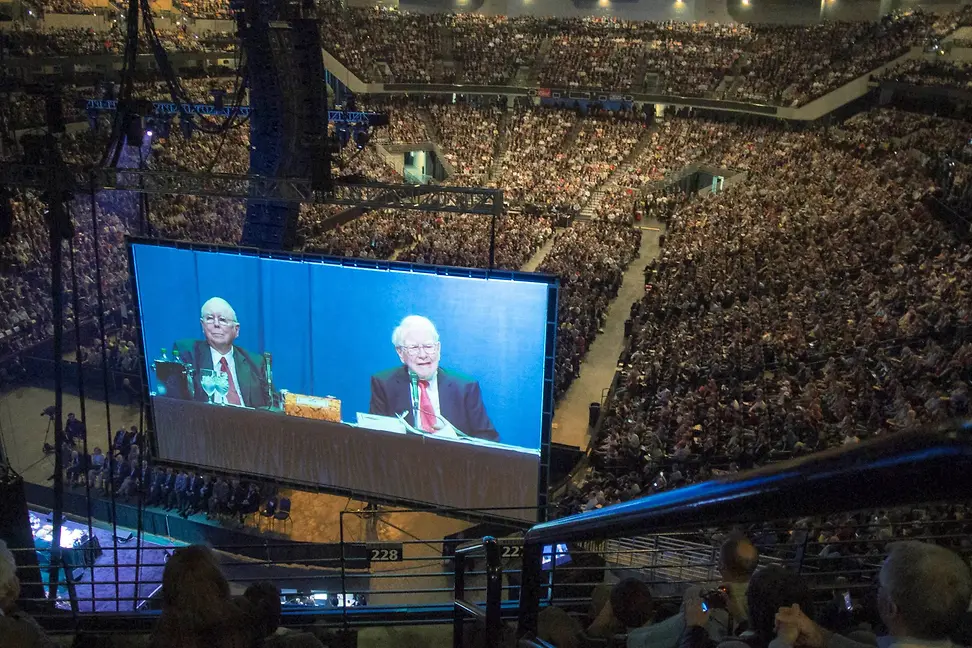

What does Warren Buffett do when he doesn't know where to put his money? The answer is simple: if there's no bargain to be found on financial markets, he buys back shares in Berkshire Hathaway, the conglomerate he runs (he's also one of its largest shareholders). And they're not cheap: at USD 621 000 a pop, the company's Class A shares are the most expensive shares in the world.

In the first quarter of 2024, Berkshire Hathaway repurchased shares for USD 2.6 billion. And with around USD 450 billion of net cash positions remaining, it's safe to assume further large-scale buybacks will be announced soon. Buffett hinted as much at the company's Annual General Meeting (aka the Woodstock for capitalists) this spring.

Buffett has long been a cheerleader for buybacks - and his message hasn't fallen on deaf ears. A whole slew of companies, from Apple to Zurich Insurance Group, have launched new share buyback programmes this year, and full-year share repurchases are expected to be record breaking. So why the sudden boom?

If a company is flush with cash and wants to create value, it only has three options to choose from. One: it can invest the excess funds. Two: it can pay dividends. Or three: it can buy back its shares. If the company repurchases and retires shares, its earnings are spread across fewer shares, thus increasing earnings per share. In theory, this will cause the share price to rise, which benefits shareholders and doesn't incur taxes the way a dividend payment would. Why? Because in many countries, capital gains are not subject to tax or are taxed at a lower rate.

Buffett's buyback criteria

So can share buybacks really deliver these positive effects? They can. Companies with a share buyback programme often enjoy above-average share price performance. This is backed up by a number of international studies. And by the S&P 500 Buyback Index, which tracks the top 100 stocks with the highest buyback ratios in the S&P 500. Overall, the Buyback Index has outperformed its benchmark index over the past 20 years. But while buybacks often do lead to a share price increase, they don’t guarantee it.

That depends instead on how credibly the company communicates and executes its share buyback programme. Take Warren Buffett. He's probably the most credible investor in financial markets. So if he announces a buyback programme at Berkshire Hathaway, the message received by the market is that the company has a significant amount of excess cash, and that he's convinced Berkshire Hathaway is a better investment than other companies.

Buffett believes that companies (including Berkshire Hathaway) should only repurchase their stocks if they meet two main criteria. First, they should have plenty of cash. Criteria number two is that their shares should be trading below their intrinsic value. Determining whether the first criteria is met is relatively easy. However, companies need to be careful when it comes to intrinsic value, because like most other indicators, it's calculated based on a number of assumptions.

Timing is key

One thing that is guaranteed to torpedo the success of any share buyback programme is bad timing. The once mighty General Electric learned this the hard way. GE's problems started during the 2008 financial crisis, and it only just managed to turn the corner - thanks in part to a cash injection from Warren Buffett.

However, this "near-death" experience didn't stop GE from quickly resuming its share buyback activities - which were often ill-timed and executed at inflated prices. Eventually, its equity base melted away and the rating agencies started to downgrade GE's credit rating. In 2018, management pulled the emergency brake and halted the buybacks - but it was too late. What had once been the world's most valuablecompany was dropped from the Dow Jones. And in April of this year, GE completed its split into three independent, listed companies: GE Aerospace, GE Vernova and GE Healthcare, marking the end of what was once one of the world's biggest conglomerates.

As an investment company, the rules are a bit different for Berkshire Hathaway than for most other companies. Which is why manufacturers who decide to follow Buffet's lead and announce a buyback programme lay themselves open to significant criticism. For example, the company's management could be accused of lacking the vision to make meaningful investments in the company's core business. Or of looking to boost the share price instead of using profits to safeguard jobs and invest in employees.

One of the world's most prominent buyback naysayers is President Joe Biden.The US has a history of being critical of buybacks: from the time of the Great Depression until 1982, they were considered a form of market manipulation and were largely prohibited. Last year, President Biden continued this tradition by pushing through a one per cent tax on share buybacks levied on companies, which he now wants to increase to four per cent. Why? To motivate companies to invest in research instead of their share price.

But government intervention isn't necessarily the answer. After all, companies with a clear growth strategy are generally happy to reinvest their profits, and don't need any prodding. Take the Swiss sports shoe manufacturer On. Business is booming - but it doesn't pay dividends or buy back its shares. This would suggest that companies playing the long game should have the freedom to decide if and when they want to invest in future business opportunities - or if they prefer to distribute their excess cash to shareholders.

Economic illiteracy

If asked what's preferable for Berkshire Hathaway, Warren Buffett would undoubtedly say that buybacks are vastly superior to paying dividends because they give the company the flexibility to react to market developments and its specific situation. He would also point out that companies should be wary of introducing a dividend policy because any cuts made to the dividend further down the road will be mercilessly punished by investors.

So let's give the Oracle of Omaha the last word, taken from Berkshire Hathaway's latest annual letter to shareholders: "When you are told that all repurchases are harmful to shareholders or to the country, or particularly beneficial to CEOs, you are listening to either an economic illiterate or a silver-tongued demagogue …".

Investment advisory

Individual advice for high-net-worth clients

Do you follow international financial markets and prefer to make quick, well-informed investment decisions yourself? We can proactively provide you with ideas and proposals from the wide-ranging experience and expertise of our investment specialists and advisors, but you make the final portfolio decisions. We monitor and report to you regularly, allowing you to actively manage your portfolio in line with your investment philosophy.

About the author

Stephan Lehmann-Maldonado, guest author

Stephan Lehmann-Maldonado is an experienced investment writer and qualified commercial teacher who, as co-owner of a communications agency, also trains young apprentices.

Market fluctuations are normal and largely unavoidable, but are they also something to fear?

Investment strategy

Recession fears recede, but geopolitics looms large

The global economy has shown remarkable resilience this year, however inflation remains higher than expected, which has led to a re-evaluation of interest-rate forecasts. Turbulence in geopolitics will likely continue, posing difficulties for both financial markets and the world's economy.

Investment strategy

How to protect yourself against AI-fuelled misinformation

Artificial intelligence makes it increasingly hard to filter information when making investment decisions. This could lead to disastrous consequences. Fortunately, there are ways to counter the AI challenge and ensure safe outcomes.

We collect and process your data on this site to better understand how it is used. In doing so, technically essential cookies are necessary in order for the website to operate and store certain settings or security-related functionalities. Please select your preferred option to continue: further details can be found in our

AnalyticsWe'll collect information about your visit to our site. It helps us understand how the site is used – what's working, what might be broken and what we should improve.

MarketingMarketing cookies allow us to display more relevant ads on external partner websites (e.g., news portals, social media platforms) based on your interests. These cookies help us measure the success of our campaigns and ensure that the ads you see are personalized to match your preferences.

External MediaContent from video platforms is blocked by default. If cookies from external media are enabled, access to such content no longer requires manual consent.