Until recently, it has been very quiet on the topic of inflation in the developed world for several decades. When it became the subject of attention, it was because there were fears of a slide into a disinflationary environment or even deflation. Important drivers of persistently low inflation in recent years have been:

subdued economic growth with a balanced relationship between supply and demand

digitalization led to continuous productivity increases

globalization enabled low-cost production of labor-intensive goods in low-wage countries

the aging population in the developed world had an overall deflationary effect: while people initially consume more on an ongoing basis in their youth, they tend to spend more frugally in old age while they face higher healthcare costs at the same time.

The current December inflation readings of +6.8% in the U.S. and +4.9% in the euro area were well above the modest averages of recent years; in the U.S., they were even the highest since 1982 (see chart 1). Even Switzerland recorded higher inflation by its standards at +1.5%. This deserves some attention.

Chart 1: U.S. inflation near a 40-year high (in a y-o-y comparison) Source: U.S. Bureau of Labor Statistics, Bloomberg, LGT

Why is inflation suddenly appearing?

The Corona pandemic set several stones in motion that have significantly upset the balance of power between supply and demand. The causes of the newly burgeoning inflation lie in a complex interplay of several factors:

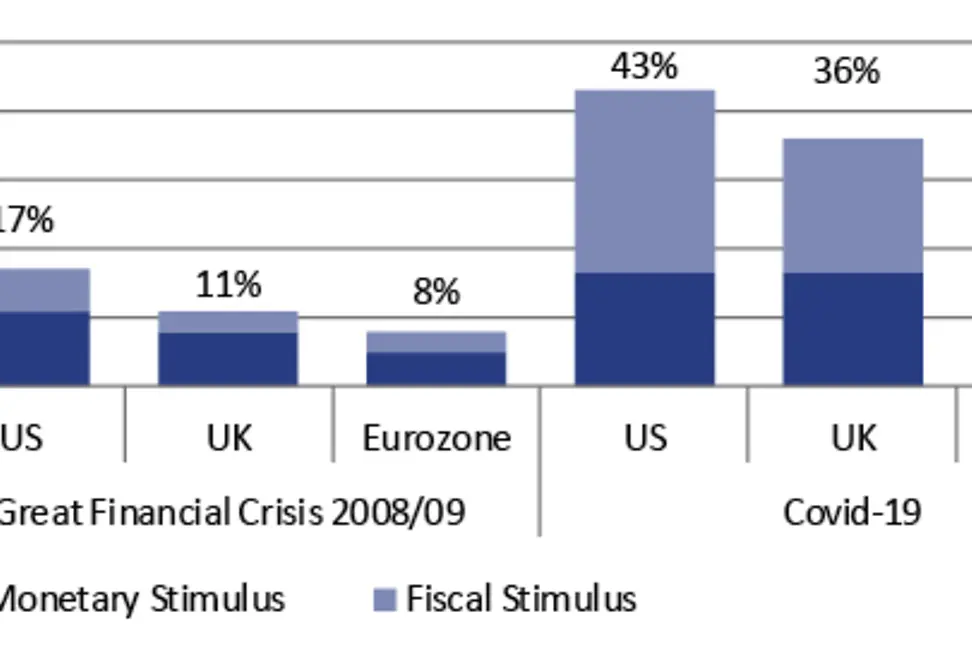

unprecedented monetary and fiscal policy measures: since the outbreak of the Corona pandemic, more than USD 30 trillion in relief measures have been launched worldwide. In the U.S., monetary and fiscal policy support amounted to 43% of GDP, about two and a half times as much as during the great financial crisis of 2008/09. In the eurozone, this figure reached about 39%, almost five times as much as during the great financial crisis (see chart 2). The otherwise extremely liberal U.S. labor market was cushioned with such generous wage loss compensation that lower income brackets at times received more compensation than lost wages.

"Lockdowns": These had different effects. On the one hand, on the supply side, complete mines, factories and port facilities repeatedly came to a standstill as a result of corona outbreaks, leading to a price-driving supply shortage. On the demand side, in turn, consumer savings rates skyrocketed because consumption of various services such as travel, eating out or going to the movies was denied.

economic reopening: The use of Corona vaccines heralded a gradual economic reopening. A huge, pent-up consumer demand began to unfold in the developed world, while recurring waves of infection repeatedly crippled production and supply chains in emerging markets.

global supply bottlenecks: the corporate world was not prepared for such a rapid surge in demand. On the one hand, inventories were reduced to a minimum as a result of the high level of uncertainty surrounding the pandemic; on the other hand, global value chains, which were otherwise highly optimized and perfected for "just-in-time," came to a standstill. Missing components such as microchips, which had been in above-average demand for home office upgrades during the pandemic, were now missing for the revived demand for cars, coffee machines and vacuum cleaners. The biggest bottleneck, however, was transportation. Freight rates rose massively, while delivery times became much longer due to "congestion" in unloading ship cargo and a lack of truck drivers.

As a result of the gap between supply and demand, prices for scarce goods - e.g. microchips - rose significantly. Transportation costs rose to unprecedented levels, and labor costs for urgently needed truck drivers skyrocketed. As a result of the stalled production of new cars, car rental companies such as Hertz and Avis in the USA, for example, were unable to renew their fleets, so they used existing vehicles for longer. This in turn caused bottlenecks on the used car market, whereupon the prices for used vehicles shot up.

Chart 2: Stimulus measures during the Great Financial Crisis and the Covid-19 pandemic, in % of GDP (Source: BNP Exane, Bloomberg, LGT)

What does higher inflation mean for equities?

The stock market feels most comfortable with moderate, stable inflation. Historically, the highest valuation multiples are paid in such an environment because the reliability of earnings estimates is high and uncertainty is correspondingly low. In a rising inflation environment, three key factors have a negative impact on the stock market, with a time lag:

inflation as a risk factor for operating margins: higher material, labor and transportation costs pose a risk to companies' operating margins, especially when firms' pricing power does not allow them to pass on higher costs directly and fully to consumers. So far, companies have shown amazing resilience in this regard.

inflation as a higher uncertainty factor: because investors do not know whether, to what extent and how quickly companies will be able to pass on higher costs to their consumers, forecast uncertainty regarding future earnings estimates increases. Higher uncertainty usually also means that investors demand a higher risk premium, which in turn is reflected in lower price/earnings ratios (P/E). In an environment of rising inflation, therefore, valuation multiples usually fall.

central banks' response to inflationary pressures: The massive monetary and fiscal policy stimulus has not failed to have the desired effect of stabilizing investor and consumer confidence and reviving demand. Central banks are now switching their policies from growth promotion to inflation control. The U.S. Fed is already scaling back its monthly quantitative easing measures, with rate hikes likely to follow later. More restrictive liquidity provides less support for risk assets such as equities, while higher interest rates in the cross-asset investment strategy make fixed income relatively more attractive.

Sector-level implications

Initially, when inflation picks up, stocks of companies in the consumer sector often carry increased risks. In the consumer staples, for example food producers, higher purchasing costs for cocoa, cereals and packaging materials have an impact. In the consumer discretionary sector, the traditional, labor-intensive retail trade, hotels and restaurants, and in the industrial sector, e.g. logistics, are affected to an above-average extent by rising labor costs. Within these sectors, pricing power and strong branding are therefore very important in order to be able to implement price increases without compromising sales. Investors should therefore focus on companies with strong pricing power, which generate high revenues per employee, offer high added value for their customers and have a strong brand. Relatively immune to inflation are technology companies, luxury goods manufacturers, and oil and energy suppliers.

However, as soon as the central banks tighten the monetary screws and interest rates rise, the situation is slightly different. Companies from so-called "mature" sectors then become less attractive. Such companies often have below-average growth rates and above-average dividend payments and are therefore regarded as "bond substitutes" respectively “bond proxies”. For such shares, interest rate increases mean that the "excess yield" of the dividend relative to interest rates declines. Among other things, stocks from the utilities, telecommunications and, in some cases, consumer staples sectors are affected. Furthermore, highly valued growth companies often also come under pressure because the present value of their future earnings declines with a higher discount factor, a reverse "compound interest" effect, so to speak.

However, there are also sectors that benefit from rising interest rates. These include in particular financial stocks such as banks and insurance companies, but also companies with constant dividend growth, which can at least defend the "dividend advantage" over interest rates or possibly even continuously improve it.

Moderate easing in sight

In view of the current inflation trend, has the time come for equity investors to make massive adjustments to their sector weightings? We believe that now is not the time to take extreme positions. A moderate overweight in financials seems appropriate, while in the other sectors, attention should be paid to the quality characteristics of a strong brand, high added value and correspondingly high pricing power. Although overall inflationary pressures are likely to persist for some time, we believe that the highest rates of price increases are in sight, after which a moderate easing should set in. The reasons for this are as follows:

Flattening economic growth: the V-shaped recovery so far has been unique in its extent and speed. Economic growth and thus inflationary pressures will slow down next year.

Shift in demand: The economic recovery to date has been driven to an above-average extent by goods consumption. In the USA, for example, around 15% more goods were consumed in 2021 than before the pandemic. We now expect a shift in pent-up demand toward services, where supply bottlenecks currently play a minor role.

Living with Corona: There is currently a great deal of uncertainty surrounding the new variant Omicron. Nevertheless, we are at a different point today than we were a year ago. More than 8.3 billion vaccine doses have been administered worldwide, which should at least protect against severe courses. In addition, adaptations of vaccines against the new variants of the virus are under development. We also expect to see an increasing number of new drugs that should contribute to a milder course of the disease in the event of a corona infection. Interruptions to production and supply chains due to widespread lockdowns should therefore decrease in the course of 2022.

Seasonal easing: We are currently heading into the seasonally above-average demand during Christmas season and Chinese New Year, after which demand should ease somewhat.

Ongoing technologization/digitalization: This has a continuous deflationary effect.

Market information from our research experts

LGT’s experts are always busy analyzing global economic and market trends. Our research publications on the international financial markets, sectors and companies will help you make informed investment decisions.

Related

金融市場

Unleashed: The monetary order since the end of the gold standard

50 years of moving away from the gold standard: Senior Economist Johannes Oehri (LGT Capital Partners) reviews monetary policy and looks ahead.

We collect and process your data on this site to better understand how it is used. In doing so, technically essential cookies are necessary in order for the website to operate and store certain settings or security-related functionalities. Please select your preferred option to continue: further details can be found in our

AnalyticsWe'll collect information about your visit to our site. It helps us understand how the site is used – what's working, what might be broken and what we should improve.

MarketingMarketing cookies allow us to display more relevant ads on external partner websites (e.g., news portals, social media platforms) based on your interests. These cookies help us measure the success of our campaigns and ensure that the ads you see are personalized to match your preferences.

External MediaContent from video platforms is blocked by default. If cookies from external media are enabled, access to such content no longer requires manual consent.